us germany tax treaty limitation on benefits

Sourced income made to foreign persons. There are certain objective tests that must be met to avoid a 3rd party country participant from exploiting the treaty benefits.

What Is Difference Between Nri And Nre Account Nri Saving And Investment Tips Savings And Investment Accounting Investment Tips

1 4 DTC USA allows the USA to tax their own citizens regardless of the provisions of the DTC.

. The US-UK competent authority agreement on Brexit confirms that post-Brexit a UK resident is a resident of a Member State of the European Community for purpose of. What is a Limitation on Benefits LOB Provision in Tax Treaty. This means that a US citizen who lives in Germany will be taxed in Germany because of tax residence and in the US because of citizenship.

The saving clause Art. The United States is a party to numerous income tax treaties with foreign countries. The complete texts of the following tax treaty documents are available in Adobe PDF format.

Y is wholly owned by X a German resident company that would not qualify for all of the benefits of the US-Germany income tax treaty but may qualify for benefits with respect to certain items of income under the active trade or business test of the US. In most cases the US will credit the German tax against the US tax Art. Treasury but that could have dramatic consequences for entities currently claiming the benefit of US.

23 5 DTC USA. R3s base eroding payments must be less than 50 50 x 100. Notwithstanding the provisions of Article 28 Limitation on Benefits a United States company or organization operated exclusively for religious charitable scientific educational or public purposes shall be exempt from tax by the Federal Republic of Germany in respect of items of income if and to the extent that a such company or organization is exempt from tax in the.

Tax Treaty Limitation on Benefits LOB Form W8-BEN-E. In order to qualify for benefits under an income tax. LIMITATION ON BENEFITS The IRS is aware of these triangular treaty provisions and therefore limits the benefits available by requiring certain requirements in order to qualify for treaty benefits.

Among the revenue provisions of the Act is one to restrict in certain cases the use of tax-treaty benefits by foreign firms with operations in the US. If the foreign person qualifies for benefits under an income tax treaty with the US the withholding tax rate may be reduced. The affordable Health Choices Act of 2009 HR 3200 promotes health care reform.

Resident company Y owns all of the shares in a US. For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. Residence alone however is not sufficient.

R3 made a deductible payment of 100 to an ineligible person R1. These are residents of a country within the EU or NAFTA that qualify under a different treaty with the UK or US and that treaty has the same terms as. PROVISIONS RELATING TO WITHHOLDING TAX LIMITATIONS ON US.

WITHHOLDING TAX ON DIVIDENDS. In order to enjoy the benefits of a US. The anti-triangular provision provides that the tax benefits that would otherwise apply under the treaty will not apply to any item of income if the combined aggregate effective tax rate in the residence State and the third state is less than 60 percent of the general rate of company tax applicable in the residence Germany.

If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. While US tax treaties are very comprehensive on many different types of tax matters it is also important to note that there are many crafty taxpayers who are masters at. Income tax treaty a person must satisfy a number of requirements including residence in one of the treaty countries.

The Germany-US double taxation. This alert concerns one discrete issue that has not yet been decided by the US. In order to meet the ownership test more than 90 of the aggregate vote and value of all the shares of the corporation and at least 50 of the vote and value of any disproportionate class of shares must be owned directly or indirectly by qualifying persons or persons.

The protocol amends the treaty to provide for Canadas first limitation on benefits LOB provision in any of its tax treaties. When it comes to real property income the Germany US Tax Treaty provides that any income generated from the real property situated in one of the contracting states may still be taxed in that state in other words for example if a US person resides in the United States and has an income generated in Germany then Germany can still tax the income even though the person is. Tax treaties then can provide significant benefits to corporations in numerous situations including the financing scenario described here but treaty rules are complicated and compliance is.

The purpose of the Germany-USA double taxation treaty. For example a foreign corporation may not be entitled to a reduced rate of withholding unless a minimum percentage of its owners are citizens or. Whether the United Kingdoms withdrawal from the European Union means that UK.

Shareholders will no longer be considered equivalent beneficiaries for purposes of the. Withholding tax applies to payments of US. International tax treaties a re designed to facilitate tax compliance between the two contracting country parties to a specific tax treaty agreement.

The double taxation treaty or the income tax agreement between Germany and the United States of America entered into force in 1990 and it serves as an instrument for the abolition of double taxation on income earned by US and German residents who do business in both countries. I resident in a third country which has a comprehensive income tax treaty with Canada or the US. Germany - Tax Treaty Documents.

On September 21 2007 Canadian minister of finance Jim Flaherty and US secretary of the Treasury Henry Paulson signed the fifth protocol the protocol to the Canada-US Income Tax Convention the treaty. The United States is very concerned about treaty shopping. Generally a 30 US.

Limitation on benefits clauses are drafted with the intention of avoiding treaty shopping whereby a third-party national or corporation sets up a shell company in a contracting state through which income will be passed by the owners in an attempt to achieve a minimal tax rate or to eliminate tax on the income altogether with no expense or real investment. If that is the case the US-German tax treaty as modified by the new Protocol the Treaty generally will be effective for withholding tax on payments made after December 31 2006 and for income taxes for taxable years beginning after December 31 2006. The USUK tax treaty includes in Article 23 a limitation of benefits provision that is intended to prevent treaty shopping by residents of third countries attempting to obtain benefits under the treaty.

R1 is an ineligible person because R1 and R3 are connected. The proposal would amend section 894 of the Internal Revenue Code code relating to income affected by a treaty. The first of these tests is that at least 95 of your shares and value is owned by 7 or fewer equivalent beneficiaries.

Treaty benefits would likely not be available to the German company under the LOB rules in that scenario and the arrangement would not result in the desired tax reduction. Limitations on benefits provisions generally prohibit third country residents from obtaining treaty benefits.

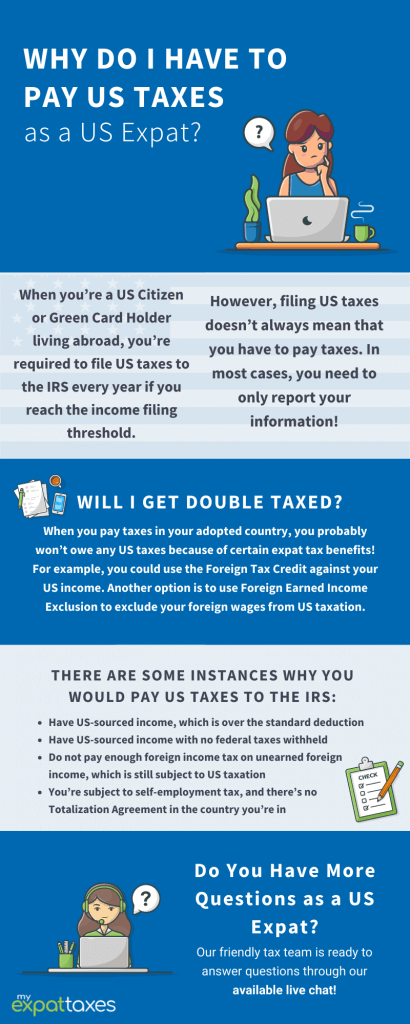

Paying Us Expat Taxes As An American Abroad Myexpattaxes

How A Non Resident Can Use A Tax Treaty To Eliminate The U S Tax Consequence Of Withdrawing Money From An Ira Or 401 K Plan Sf Tax Counsel

Form 8833 How To Claim Income Tax Treaty Benefits

Tax Free Withdrawal Of Us Based Retirement Funds Sf Tax Counsel

The Us Uk Tax Treaty Explained H R Block

Everthing Us Taxes For Americans Abroad Myexpattaxes Tax Experts

2

India S Dtaa Regime A Brief Primer For Foreign Investors

Paying Us Expat Taxes As An American Abroad Myexpattaxes

Germany Entitlement Of A Us S Corporation To Benefits Under The Germany Us Tax Treaty International Tax Review

Claiming Tax Benefits Under Dtaa Ipleaders

2

United States Germany Income Tax Treaty Sf Tax Counsel

Form 8833 How To Claim Income Tax Treaty Benefits

Minister Of Finance Approves Increase In Withholding Tax Rates Under Double Taxation Agreements Between Nigeria And Other Countries With Effect From 1 July 2022 Withholding Tax Nigeria

2

2

The Estee Lauder Companies Inc 2008 Annual Report

Expats In Canada Expat Tax Professionals